All articles

AI's Goal in Banking is a Better, More Seamless Customer Journey

Gabriel Ryan, VP in the Risk Management Group at DBS Bank, explains how banks are cautiously implementing AI.

Make CX Current News one of your go-to sources on Google

With AI, both customer experience and efficiency gains should go hand in hand. They are not in an adversarial relationship. A bank's KPIs should include fewer customer complaints about the bot giving bad advice and fewer requests from users to drop off and speak to a live agent.

Gabriel Ryan

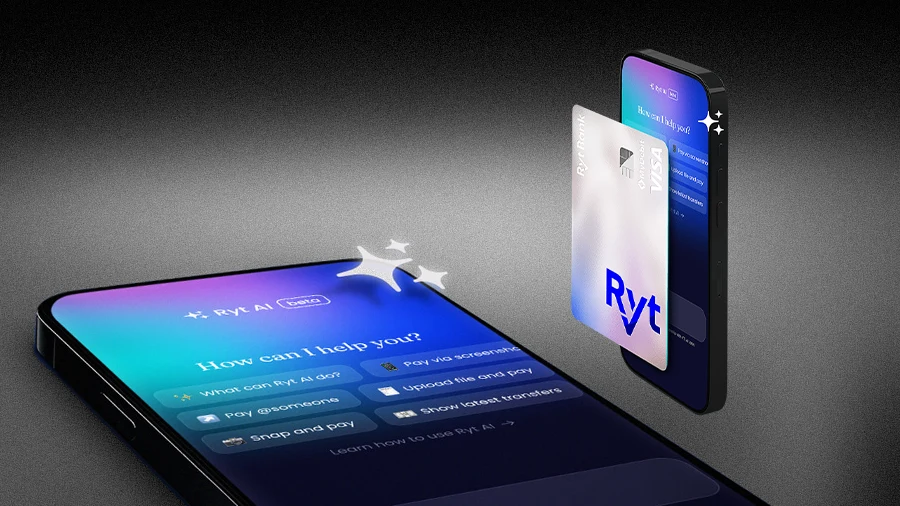

Banks and fintechs are racing to deploy AI, but they're running into a fundamental conflict. The promise of seamless automation is crashing into the messy reality of cautious implementation. In Southeast Asia, a new AI-powered bank, Ryt Bank, lets users send money by typing or speaking instructions, but the AI only prepares the transaction for the user's final confirmation. Finding the right balance of human to AI right is crucial. Misjudge it, and you risk becoming the next cautionary headline.

To understand how AI is shaping the future of banking, we spoke with Gabriel Ryan, a Vice President in the Risk Management Group at DBS Bank and former senior leader at financial institutions like Standard Chartered Bank, Maybank, and EY. As a Certified Financial Risk Manager (FRM), he shares how banks are preparing for what tomorrow's customers will want and deserve.

A helpful co-pilot: Instead of aiming for full automation, the initial strategy is more practical: let AI assist, but keep humans in control. This approach works as a safeguard by having the technology prepare transactions, leaving the final say to the user. "What the bot does is prepare the transaction for the user to confirm. The AI does not immediately perform the instructions. It only prepares them up to the final step. This is a key mitigating factor, as the AI doesn't have the ability to directly execute transactions, at least not yet," he explains. "If the AI cannot understand instructions because a user types in colloquial language or shorthand, it defaults to a manual option," he adds. "I think this is a pretty good start for rolling out AI within this context."

According to Ryan, banks are approaching AI on a "complexity spectrum." Simple tasks are seen as low-hanging fruit, while more complicated, advisory functions represent a much higher-stakes application. "For certain banking tasks, like payments, it should be relatively straightforward," he said. "It shouldn't be a complication for generative AI systems to comprehend instructions in a natural language manner and at least prepare the transactions."

It becomes more complicated when AI is used to provide investment advice, Ryan says. In that case, a lot more caution and testing is needed to ensure the advice is sound and according to the bank's internal standards. He points to the Air Canada case, where its bereavement-policy chatbot confidently provided incorrect information to a customer. "We don't want a similar case in the banking sector," he cautions.

New tech, old rules: So how do you manage a brand-new risk? As it turns out, with a familiar playbook. "Since many generative AI systems are external models from tech companies, they should be treated as a third-party risk. This is a well-understood area of risk management within banking, so it's just applying that existing third-party risk framework to the AI space," Ryan explains. This rigorous approach stems from both internal policies and external regulatory pressures that mandate strict oversight of third-party vendors in the financial sector.

Hand in hand: For him, this intense focus on risk and customer satisfaction is a direct path to better business outcomes. A successful AI strategy treats customer experience and internal efficiency as linked objectives, where improvements in one area drive gains in the other. "Both customer experience and efficiency gains should go hand in hand. They are not in an adversarial relationship," Ryan says. "The KPIs should include fewer customer complaints about the bot giving bad advice and fewer requests from users to drop off and speak to a live agent."

AI is the next logical step in a multi-decade journey to improve the user experience, suggests Ryan. He traces a direct line from the friction of the past to the seamless potential of the future. "Throughout the evolution of technology in banking, the goal has always been to improve the customer experience," he says. "We went from standing in long queues at a branch, to the advent of the ATM, to web-based banking, and then to mobile apps." This evolution also saw the rise of peer-to-peer payment services like Venmo and Zelle, further streamlining transactions. "Today, we have GenAI to do that for us. It's a clear evolution of improving the financial services experience."

His personal prediction for the next step in the banking evolution is truly hands-free banking. He envisions a future where users could ask for an analysis of the day's market and receive automated advice on what to do next. "That might be something we see in the coming days," he imagines. But as AI pushes toward this future, it remains grounded in a cautious present. Managing risks like "hallucinations, fairness, and the fair use of AI" is a real and active concern that Ryan says is "top of the agenda for most banks." We are not yet at a point where AI can be fully trusted to perform 100% of our transactions, and perhaps wisely so. The journey, with its inherent challenges, is just beginning, but banks are methodically working towards a future where AI acts as a seamless, value-adding financial assistant, always balancing innovation with trust.